Why Invest for College Fund?

College Costs Increase

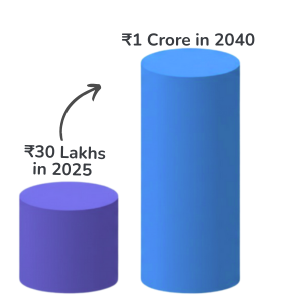

A college degree costing ₹30 lakhs today will cost ₹1 crore in 2040

Maintain Separate College Fund

Separate college fund builds discipline without mixing with day to day expenses

Compounding Power

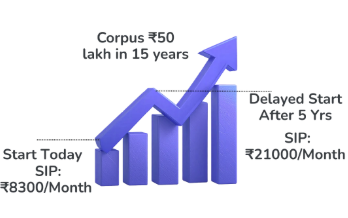

SIP today will be ₹8300 vs ₹21000 in 5 years to accumulate ₹50 lakh in 15 years. Overall contribution will be higher by ₹11 lakhs just by delay of 5 years